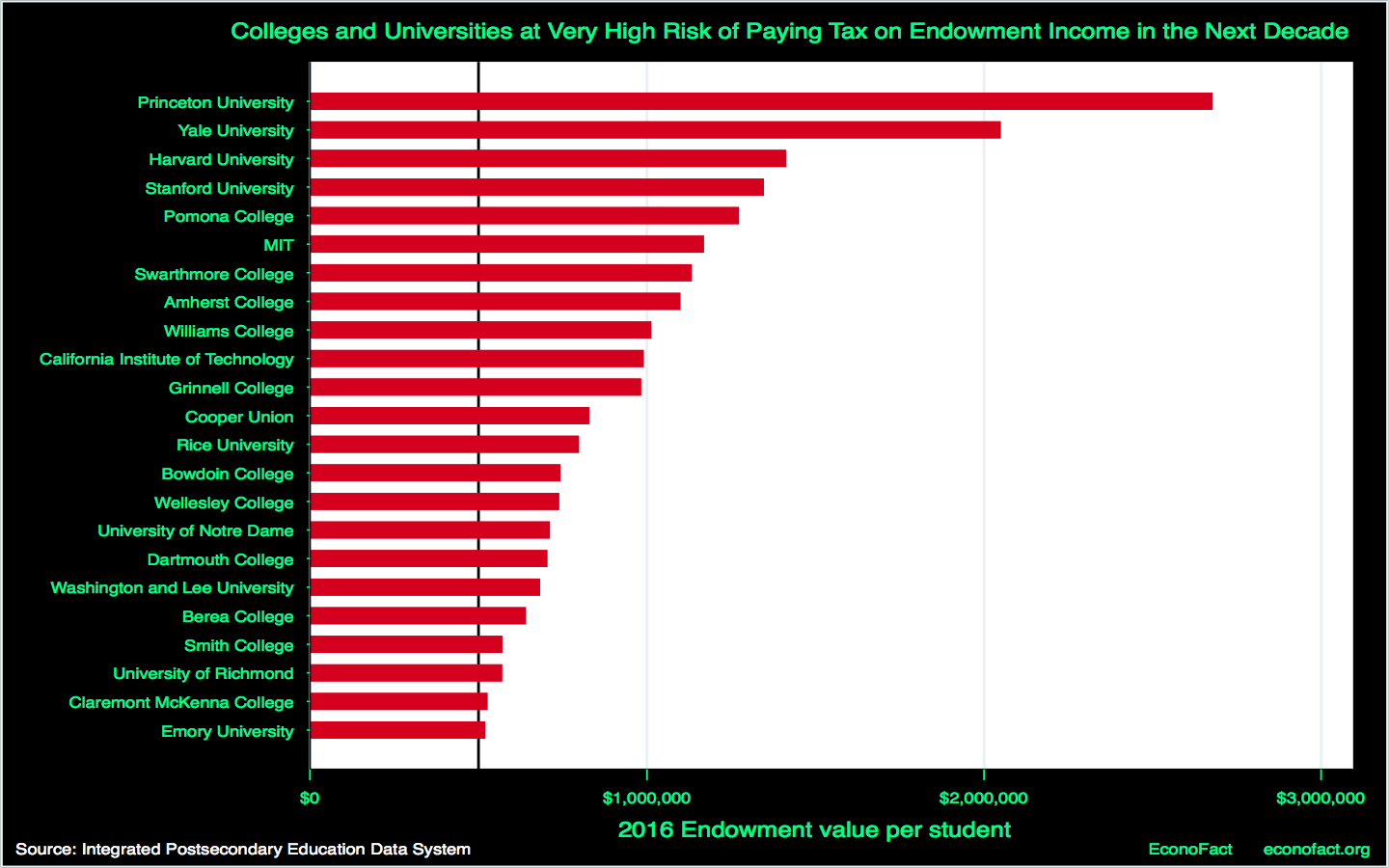

House Completes Markup of Amendment to Endowment Excise Tax (IRC 4968)

From The University Endowment Income Tax: Who Will Pay it and Why Was it Implemented?

Yawn. It’s the dog days of summer, alright. Yesterday, Ways and Means completed markup of proposed amendments to the endowment excise tax imposed by IRC 4968. Here is part of the JCT report:

Description of Proposal

The proposal modifies the asset-per-student calculation used in determining whether an institution is an applicable educational institution. Specifically, a student is not taken into account with respect to an educational institution for this purpose unless the student meets the eligibility requirements under section 484(a)(5) of the Higher Education Act of 1965.9 That section requires that the student “be a citizen or national of the United States, a permanent resident of the United States, or able to provide evidence from the Immigration and Naturalization Service that he or she is in the United States for other than a temporary purpose with the intention of becoming a citizen or permanent resident.” The proposal also requires an applicable educational institution that is required to file an annual information return (Form 990) to include on the return the number of students taken into account for purposes of the asset-per-student calculation, determined both before and after application of the rule that limits the student count to students who meet the eligibility requirements under section 484(a)(5) of the Higher Education Act of 1965.

Effective Date

The proposal is effective for taxable years beginning after December 31, 2024.

darryll k. jones