A New Zealand Solution for Charitable Hoarding

In New Zealand an RNZ report suggests that there is “about $2 billion of profit in the charitable sector that is not subject to tax.” The report is ostensibly about unrelated business income, but the further discussion regards payout rates. The Report’s implicit premise is that if a charity ends a year with an increased net asset balance, it might be hoarding rather than pursing charitable purposes. Thus, the increase should be taxed currently, perhaps with a rebate if the charity has a decrease in a subsequent year.

Deloitte tax partner Robyn Walker said the issue the government seemed concerned about was whether charities were “potentially not doing the charitable stuff on a timely basis”. “It’s hard when looking at the aggregated data – it could be that 90 percent of charities spend every cent they make and it’s only a small subset of charities which are actually contributing to that $2b difference between income and expenses.” She said charities were required to apply all their income and assets to charitable purposes. “If you apply it to the private benefit of an individual, you lose your charitable status. But what happens is that sometimes the charitable purpose might arise some time into the future. There are definitely periods where they’re not spending everything they are making because there is a longer-term purpose… there’s a bunch of different obligations they have to meet to keep their charitable status.”

Walker said it had been suggested that charities could have a sort of memorandum account where they were able to claw back the tax they paid as they spent their money on charitable purposes.

It is, of course, simplistic to think that an increased net asset balance at the end of the year means a charity is hording. Still, taxing stored and unspent charitable revenue with a provision for rebate when the revenue is and finally spent in a later year is an idea worth pursuing. A system like that would be sort of the opposite of a consumption tax. Consumption taxes encourage savings but maybe we want to discourage or at least decrease charitable savings. So for charities we would tax charitable savings and exempt current charitable consumption. We want more charitable consumption. But the current approach incentivizes savings (hoarding) and disincentivizes spending (charitable consumption).

The New Zealand proposal would require ironing out some details, but limiting exemption to actual charitable consumption could accelerate charitable spending by Foundations, the prototypical charitable hoarders. Indeed, private foundation charitable hoarding is a persistent problem worldwide. In her recent commentary Professor Brigitte Alepin calls the whole thing a “farce” of international proportions:

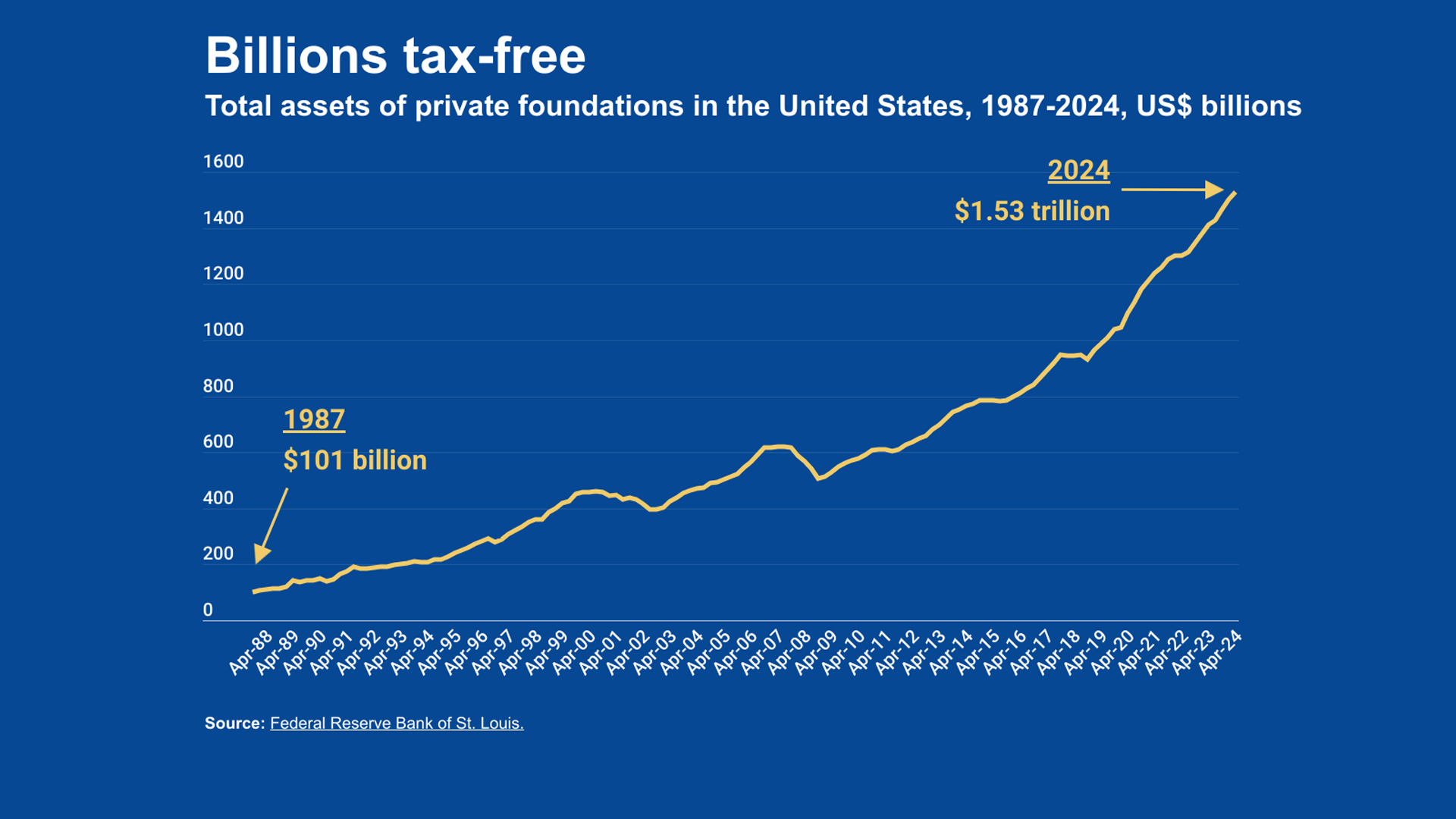

In the United States, the assets of private charitable foundations have increased 15-fold in just over 35 years. Since the start of the pandemic alone, they have soared by nearly 50 per cent. On a global scale, private charities benefit from increasingly generous tax arrangements, a lack of transparency and lax regulations. As a result, billions of dollars are multiplying tax-free, depriving governments of crucial resources to meet urgent needs. This charitable farce, also present in Canada, has been going on for far too long.

Foundations take on different forms and names in different countries, but their tax regime generally boils down to the same three components: a tax gift for the founder, a tax vacation for the foundation, and a charitable redistribution obligation, often minimal, for the foundation.

In Canada, where the tax regime for foundations is one of the most generous in the world, donations from individuals can benefit from a tax credit of up to 53 per cent of the value of the donation, the foundation is tax-exempt and only has to devote five per cent of the value of its assets to charitable purposes.

Public finances are severely penalized by this system, as it takes nearly 35 years for the value of the charitable spending carried out by foundations to exceed the value of the tax benefits enjoyed by the foundation and its founder. For donations of publicly traded securities, this period extends to around 100 years, because in addition to the donation tax deduction or credit, the donor also benefits from a capital gains tax exemption.

In the G7 countries, foundation wealth totals around US$2 trillion, a figure that could rise to US$3 trillion worldwide (my estimates). Between themselves, the world’s 10 richest private charitable foundations hold a combined wealth of almost US$500 billion. The growing popularity of foundations seems far from over. In its 2020 Tax and Philanthropy report, the Organisation for Economic Co-operation and Development (OECD) highlighted “the increasing prevalence of large philanthropic foundations has placed greater focus on the degree of influence of large donors on the use of taxpayer funds.”

Under most western laws, donors and foundations get a tax benefit today for charitable spending very much later. Like DAFs, Foundations are adept at avoiding meaningful required payouts. Ironically, the lobbying power that comes with untaxed accumulated wealth helps preserve untaxed accumulated wealth! It’s true that everybody needs a reserve. But Alperin’s implicit point is that the burden of the rainy day fund falls entirely on the rest of us and hardly at all on donors or foundations. Taxing a foundation’s annual net asset increase, with a provision for deductions for spending attributable to previously taxed wealth would better allocate the burden between the foundation and the taxpayers.

darryll k. jones