States’ Very Slow Efforts to Quantify Community Benefit Standards

From the NJ Hospital Association

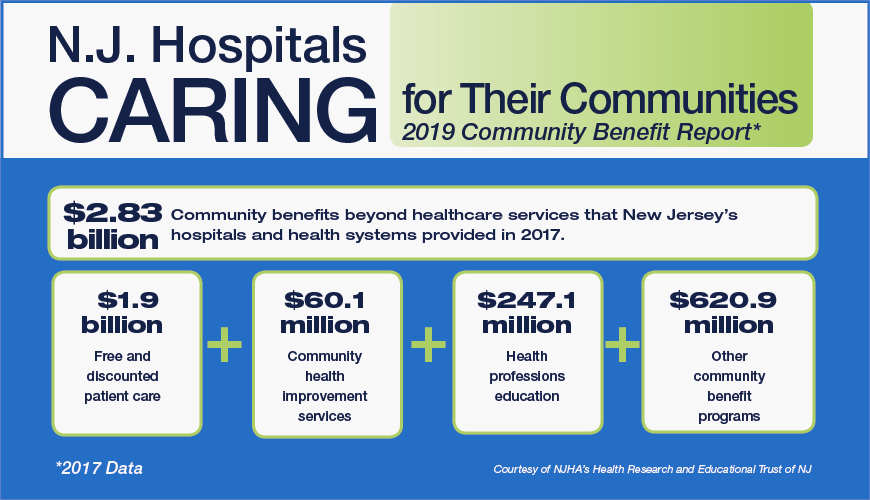

Federal law does not set a definitive level of “community benefit” nonprofit hospitals must provide in return for tax exemption so there is always room to debate whether hospitals do enough to justify tax subsidies. The states, though, seem more inclined to set quantifiable levels. Two scholars have collected data regarding the adequacy of community benefit and charity care rendered by New Jersey nonprofit hospitals, after that state set a required 12% (of total expenses) community benefit standard: Here is the abstract for An Analysis of Tax Exemption and Community Benefits for Nonprofit Hospitals in New Jersey:

The public policy rationale for granting tax-exempt status to entities engaged in select commercial activities is that their overall benefits to society outweigh the private benefits received by stakeholders. Applied to hospitals, tax-exempt hospitals are expected to render charity care, later expanded to cover “community benefits” to justify their tax exemption status. Recent evidence from several sources indicates that tax exempt hospitals frequently do not meet the simple test of the cost of charity care or community benefits exceeding the taxes foregone. We examine whether tax-exempt hospitals meet this test in New Jersey from 2016-2018. We find that an average of 24% of nonprofit hospitals did not provide more incremental community benefits than tax exemptions. This number increased to an average of 83% percent if the criteria were changed from “community benefits to “charity care.” Nonprofit hospitals contributed an average of 6.81% community benefits and-2.75% charity care after accounting for their tax savings due to their exempt status. Given these findings, we recommend reconsideration of the bill passed by the NJ State Legislature setting 12% community benefits to total expense ratio as the litmus test for nonprofit hospitals to avoid paying the state-mandated annual community service contribution, which is in lieu of property taxes to the host municipality.

Meanwhile, the Lown Institute has updated its “Hospital Community Benefit Policy Watch.” This helpful guide provides summaries of state laws defining hospital community benefit standards, with links to all 50 states. The data indicate that only 6 states impose minimum community benefit standards, though many others have reporting requirements. Most of the recent state law activities towards enforcement of community benefit is geared towards limiting nonprofit hospital debt collection practices. Here are two sample entries regarding state efforts to quantify minimum community benefit:

The Montana Department of Public Health and Human Services proposed a new rule in July 2024 to clarify the responsibilities of nonprofit hospitals “with respect to the provision of community benefits and financial assistance in the areas they serve.” The rule directs the department to collect baseline data on hospital community benefits and formulate standards based on that data, including potential fines for noncompliance. In response to a 2020 state audit of hospital community benefit performance, Montana legislators proposed a bill in 2022 that would set higher reporting standards for hospital community benefit spending. Due to opposition from hospitals, this bill was watered down and now does not require hospitals to report anything additional to what they provide the IRS.

. . .

In response to a tax court ruling that found that some hospitals were not meeting criteria for their tax exemption, NJ passed a law in February 2021 that hospitals have to pay a $3 per-bed-per-day fee to local governments to make up for property taxes they don’t pay. Hospitals contributing more than 12 percent of their operating budget to community benefit spending are exempt from the contribution.

darryll k. jones