Why is Navy Federal Credit Union Tax Exempt?

The Independent Community Bankers of America recently let be known that it cares little for the tax exemption provided to federal and state credit unions with whom ICBA members invariably compete. In an August 6 letter to Ways and Means, ICBA said this:

ICBA is encouraged by the committee’s scrutiny of tax-exempt institutions, including universities and nonprofit hospitals. These institutions are entrusted with a public mission and must be held to account by Congress when they fail in that mission.

Comprehensive tax legislation should touch all aspects of the code and include a review of all tax-exempt institutions. Notably, today’s multi-billion-dollar credit unions have outstripped their public mission and tax exempt purpose and are now even leveraging their tax-exemption to purchase tax-paying community banks. The pace of these acquisitions in recent years is driving the consolidation of financial services across all markets, to the harm of consumers and small businesses.

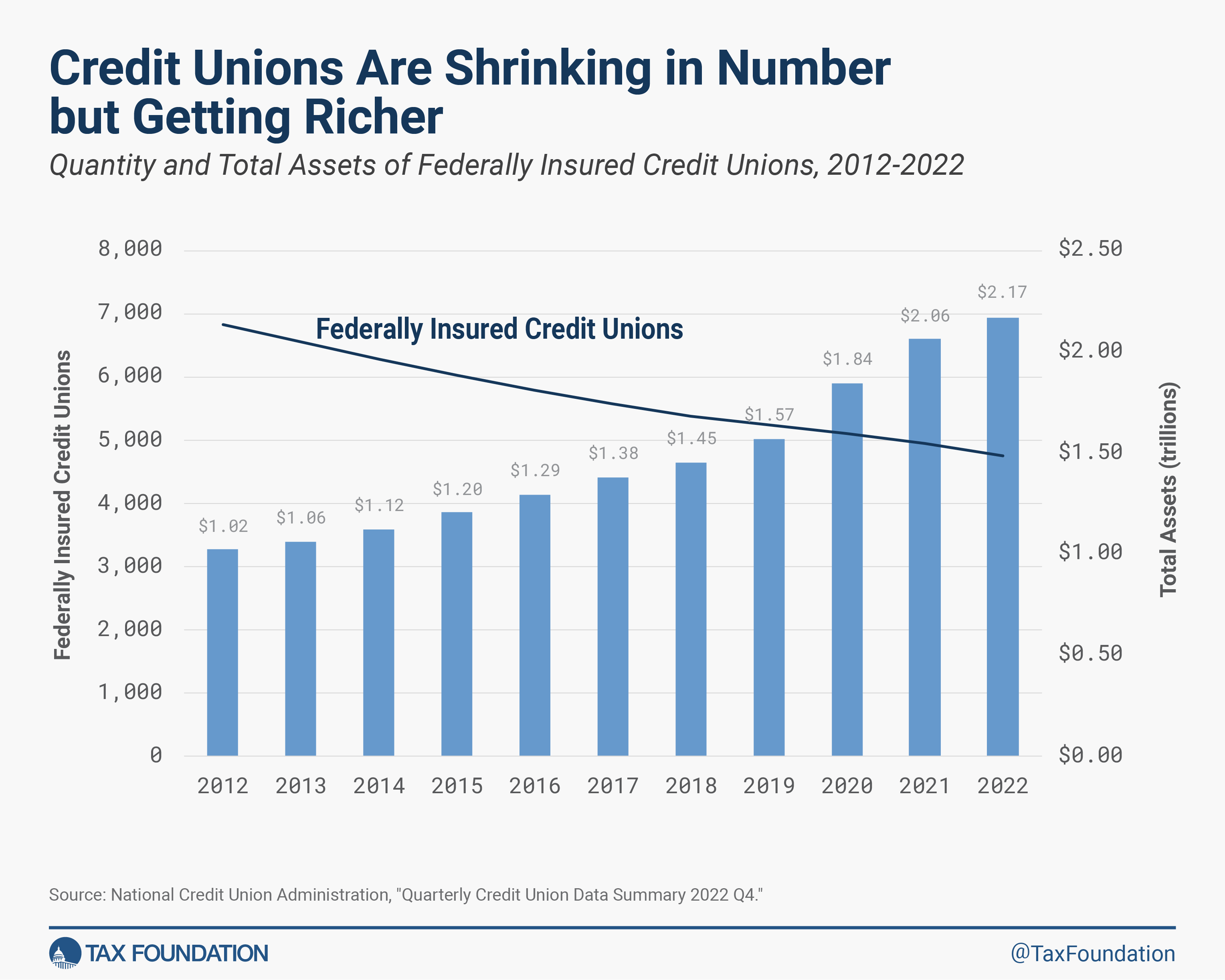

As you grapple with the cost of extending expiring tax relief, every tax expenditure should be rigorously interrogated. Modern credit unions exploit a tax exemption created to “serve people of modest means” within defined fields of membership. The largest credit union today, Navy Federal, has assets of $168 billion, dwarfing the size of a typical community bank with assets of less than $1 billion. The credit union tax exemption subsidizes multi-million-dollar executive pay, outsized marketing budgets, sports stadium naming rights, lavish headquarters, and increasingly, acquisitions of community banks rooted in their communities for decades. Field-of-membership rules, once a check on credit union expansion, have been eroded by the National Credit Union Administration to the point of meaninglessness. Credit union practices include wealth management and financing of private aircraft. Pentagon Federal Credit Union recently has partnered with Goldman Sachs to finance luxury mixed-use developments in Washington, D.C. with an $847 million loan to develop Phase II of the DC Wharf. This is not serving people of modest means.

As there is no longer any meaningful distinction between credit unions and commercial banks, we believe they should be taxed equivalently. ICBA has developed a menu of options for taxing credit unions and would appreciate the opportunity to discuss them with you.

Stokeld reports that credit unions ain’t hardly worried about a bunch of sniveling banks. And the Tax Foundation has an informative report on tax exemption for credit unions. It’s written by Scott Hodge, who is generally opposed to tax exemption for all but stereotypical nonprofits subsisting entirely on donations. Navy Federal ain’t that. Hodge makes a good argument against the continued tax exemption and nonprofit subsidies afforded credit unions. Here is a sample:

American credit unions were modeled on the “self-help financial cooperatives” started in Germany during the 1850s when poor and rural people had little access to banking or lending. The idea was for people in a community—who have a “common bond”—to combine their resources into a lending pool accessible to those in need. As Rep. Henry B. Steagall (D-AL) said in the minutes before the final vote on the bill, credit unions represent “an effort to help citizens solve their own economic problems and meet their own conditions of distress out of their own resources and by their own efforts. The system loans on character, a thing greatly to be desired.”

Steagall and other supporters were motivated by the belief that expanding credit unions would undercut the “loan sharks” and “shot-gun loan offices” that charged excessive rates on loans to the poor and working class during the Great Depression. That idealized image of credit unions did not shield them from criticism. By the 1950s, just 20 years after the enactment of the Credit Union Act of 1934, experts began asking, “Do Federal credit unions serve any useful purpose in the present-day American economy? Haven’t Federal credit unions expanded their services beyond the area visualized for them by the founders of the credit union movement? Shouldn’t the size of Federal credit unions be limited because some have grown beyond the point where they can continue to be a credit union as defined by the early philosophers of the movement?”

Credit unions may have survived those early challenges by lawmakers and business groups—who claimed that the credit unions’ tax exemption allowed them to unfairly compete with commercial banks—but the issues have not changed with time. As we will see, the competitive gap between credit unions and banks has widened in the years since. Studies now show that credit unions enjoy a taxpayer subsidy much larger than the roughly $3 billion in forgone tax revenues estimated each year. The credit unions’ own association puts the total tax and non-profit subsidy at some $21 billion annually. And despite their mandate to serve people of “small means,” credit unions are increasingly serving upper-income families, in part because that is where the profits are, but also because the number of Americans who are unbanked or underserved has nearly disappeared.

However, thanks to their special charter, federal credit unions may be the only fully private, non-religious organizations in America not required to file a tax return. Federal credit unions are considered to be “instrumentalities” of the federal government and are tax-exempt under 501(c)(1) of the Internal Revenue Code. This designation is reserved for organizations created or chartered by an act of Congress, such as the Corporation for Public Broadcasting and regional Federal Reserve banks. And because federal credit unions are exempt from filing Form 990 tax returns, they lack the kind of transparency and accountability that members and taxpayers deserve. There is no independent way of determining if federal credit unions are meeting their mandated missions. Moreover, federal credit unions are exempt from unrelated business income tax (UBIT) rules that require nonprofits to pay tax on income derived from commercial activities unrelated to the organization’s mission. Admittedly, UBIT rules have a lot of loopholes—for example, they allow college sports associations to collect millions of dollars in TV revenues tax-free—but exempting federal credit unions from UBIT gives them even more freedom to expand into businesses unrelated to serving underserved customers.

We hardly pay attention to credit unions and I bet that’s just how Navy Federal likes it.

darryll k. jones