Will Allowing TCJA Provisions To Expire Hurt Charitable Contributions?

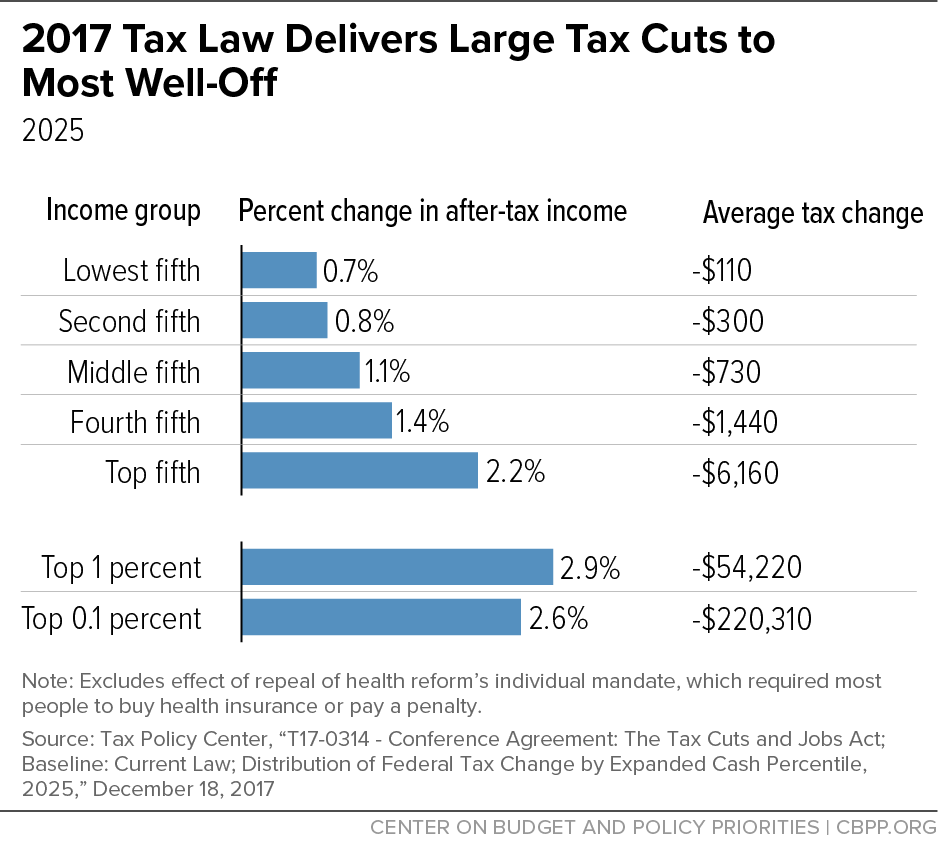

The chart pictured above and the editorial linked below prove that two things can be true. It is a logical argument the TCJA benefitted the rich most and as a result the wealthy gave more to charity. If the TCJA hurt everybody else, everybody else should have decreased charitable giving. If wealthy giving increased in an amount greater than the absolute value of the decrease, the TCJA was good and bad for charity. Good because it increased giving, but bad because it stimulated greater demand for charitable and social services by the rest of us who lost money on the deal.

So if regressive tax laws are reversed we should expect charitable giving to decrease unless the reversal stimulates giving by everybody else in an aggregate amount greater than the absolute value of the expected decrease in giving by wealthy folk. But unlike the first scenario, the outcome is only good for charity, not good and bad. Because an increase in giving by everybody else might correlate to a decrease in demand for charitable and social services. And that might be true whether everybody else steps up giving or not. In either case, they will still have more money with which to satisfy their living needs and desires. Logically, middle class taxpayers should have less demand for social services while the demand from the wealthy decreases or stays the same.

Meanwhile, Lester Salmon of Philanthropy Roundtable says this in the Chronicle of Philanthropy:

Government leaders, economists, and tax policy experts are already debating what the nation’s tax code will look like when the 2017 Tax Cuts and Jobs Act expires at the end of next year. Lost in the conversation, however, are the potential consequences for charitable giving. Tax policy is often framed as a matter of government revenue. But changes to the tax code can have profound ripple effects on philanthropy that harm communities and the nation.

That’s why some of us in the philanthropy world are deeply concerned about the coming expiration of provisions in the tax legislation — signed into law by President Donald Trump — and efforts to revert to previous tax structures. Doing so could significantly increase taxes for Americans of all incomes, ultimately dampening charitable giving. A total of 23 tax provisions are set to expire at the end of 2025, many of which helped fuel charitable giving trends in recent years. For example, the tax law temporarily increased the deduction limit on charitable contributions from 50 to 60 percent.

Additionally, by lowering the tax burden for most Americans, the tax legislation benefited philanthropy more broadly. That’s because a fundamental link exists between tax policy and charitable giving. A thriving economy translates to increased economic activity and disposable income, which fuels charitable generosity.

darryll k. jones