Nonprofit Medical Debt Collection is Big Business

We haven’t picked on nonprofit hospitals in awhile so here is something from the Nonprofit Quarterly. It is not just another list of nonprofit bad guys. Its interesting, instead, for its discussion of the ways nonprofits monetize medical debt by selling it to third parties or facilitate high interest medical debt cards. After which the third parties do all the nasty things in their own name — making it seem as though the nonprofit hospital does not engage in those nasty practices themselves:

. . .

Meanwhile, the United States is without peers internationally in the extent and depth of its medical debt crisis. Socialized healthcare in most other wealthy countries means that medical debt is minimal or essentially non-existent as a widespread issue. This past June, the international NGO Human Rights Watch condemned the current state of American medical debt, describing the situation as depriving American patients of human rights.

. . . .

“Our healthcare system is now generating medical debt on an industrial scale,” Noam Levey, senior correspondent for KFF Health News, tells NPQ. “And a good part of that is coming from not-for-profit health care,” adds Levey, whose reporting, much of it in partnership with NPR, has dug deep into the scope and depth of medical debt in the US. “Our healthcare system is now generating medical debt on an industrial scale,” Noam Levey, senior correspondent for KFF Health News, tells NPQ. “And a good part of that is coming from not-for-profit health care,” adds Levey, whose reporting, much of it in partnership with NPR, has dug deep into the scope and depth of medical debt in the US.

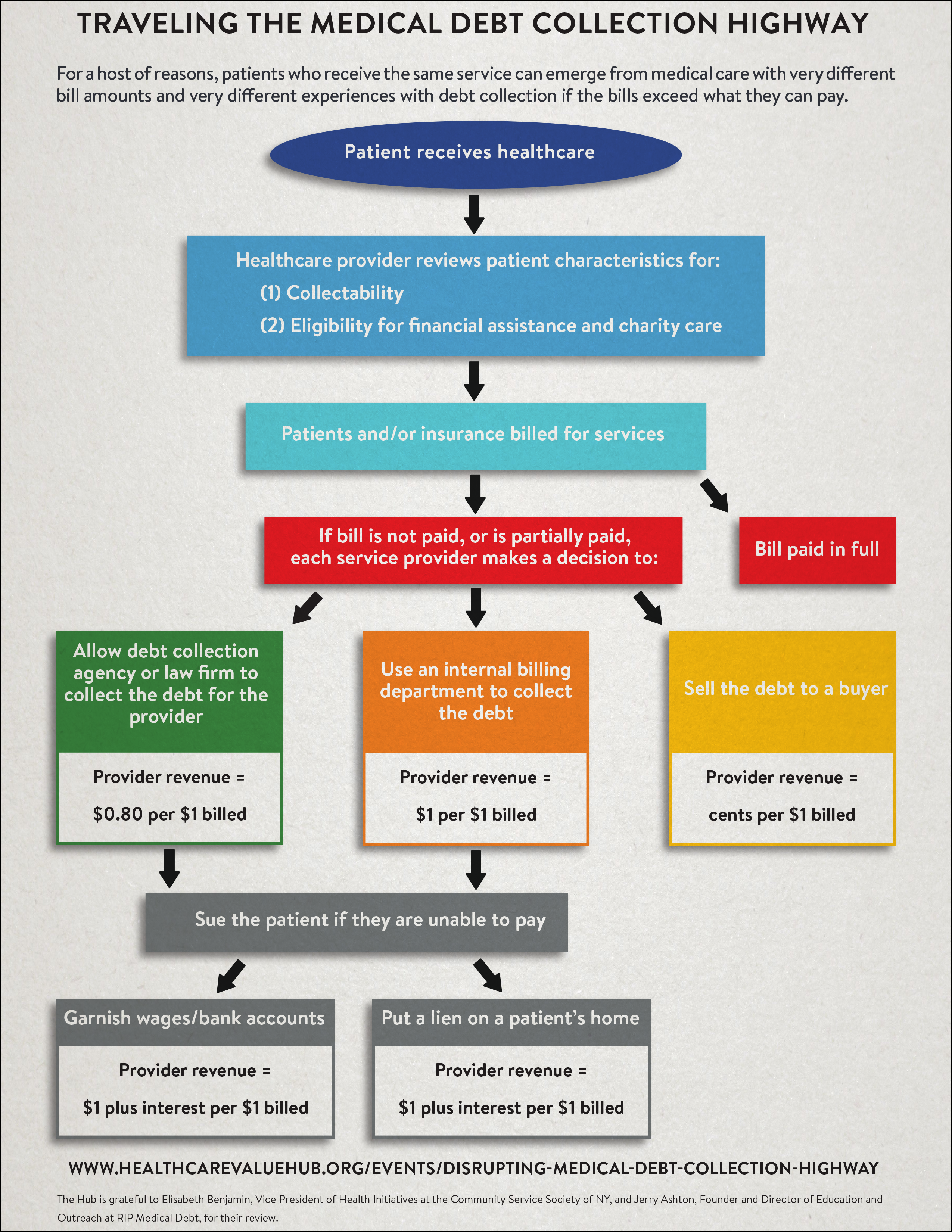

Selling patient debt to private, for-profit debt collection companies is a relatively new financial venture for hospitals, one with profound implications for the patients holding that debt. “What happens when a hospital sells patient debt is they essentially wash their hands of it—these companies buy it and then they can engage in all manner of collection activities against these people,” says Levey—all without the hospital’s name attached to such aggressive legal tactics. NCLC attorney Haynes agrees, noting that medical debt can even result in civil arrest warrants. “We’re talking about things like wage garnishment, bank account seizure, property liens on homes,” Haynes tells NPQ.

Another tactic increasingly employed by hospitals involves partnerships with third-party for-profit lending and collection companies that offer to put patients on payment plans—plans that generally come with steep interest rates and penalties. In the past, hospitals offered and handled interest-free payment plans in-house. Now, increasingly, they are only too happy to hand over responsibility for these plans to for-profit companies.

With these companies, Levey notes that “if you miss a payment or you don’t pay off the whole balance by, say, 24 months, your interest rate is going to jump up to 25 percent [or more], which is obviously huge.”

One of the latest innovations to emerge—and take advantage of the lucrative US medical debt landscape—is the rise of medical debt credit cards, often promoted and issued in doctors’ offices and hospital rooms. These offer lines of credit managed by for-profit companies and often carry severe interest rates and penalties, arrangements many have called predatory given the often-urgent conditions that could make especially low-income patients feel pressured to sign. This June, a group of Democratic senators asked the federal Consumer Financial Protection Bureau to investigate the practice of issuing such credit cards.

darryll k. jones