Circuit Split Coming Soon on Whether Tax Exemption is An Expenditure

We blogged last year about courts equating tax exemption to government spending in the context of two private schools arguing that Title IX was not applicable to them merely as a result of their federal tax exempt status. Title IX, you will recall, is triggered by the receipt of federal funding and two federal district courts ruled that tax exemption is just that, the receipt of federal funding.

We blogged last year about courts equating tax exemption to government spending in the context of two private schools arguing that Title IX was not applicable to them merely as a result of their federal tax exempt status. Title IX, you will recall, is triggered by the receipt of federal funding and two federal district courts ruled that tax exemption is just that, the receipt of federal funding.

The cases are potentially very significant for tax exemption jurisprudence because appellants and amici challenge the generally accepted notion that tax exemption is economically equivalent to government spending. We might eventually be faced with a circuit split because one case is pending before the 9th Circuit, notoriously liberal, and another before the 4th Circuit, described by some as the “most aggressively conservative federal appeals court in the nation.” I got a chance to skim through the briefs in the 4th Circuit case. Most of the briefs appear to argue that tax exemption is not what Congress intended as “financial assistance,” under Title IX. That argument, if accepted, moots the tax exemption as expenditur4e issue. It probably should be accepted, to be honest. Title IX is all about direct spending and we don’t have to disclaim tax exemption as subsidy to assert that Title IX conditions direct not indirect spending on equal opportunity. But let’s hope the courts don’t do anything stupid and decide the case on the most narrow ground possible.

One brief, submitted by the Thomas Moore Society as amicus, makes the explicit argument that tax exemption is not an expenditure:

THE INDIRECT BENEFIT OF A “TAX EXPENDITURE” UNDER THE TAX CODE FUNDAMENTALLY DIFFERS FROM ACTUAL RECEIPT OF GOVERNMENT FUNDS.

Furthermore, equating an exemption from tax under § 501(c) with direct financial payments made by the government to a participant in a federal program runs counter to the definition of making an “expenditure” through the Internal Revenue Code. For purposes of the federal budget, “[t]ax expenditures . . . [are] revenue losses attributable to provisions of Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability.” U.S. Dept. of the Treasury, Policy Issues: Tax Policy, Tax Expenditures, available at https://home.treasury.gov/policy-issues/tax-policy/tax-expenditures (last visited June 23, 2023).

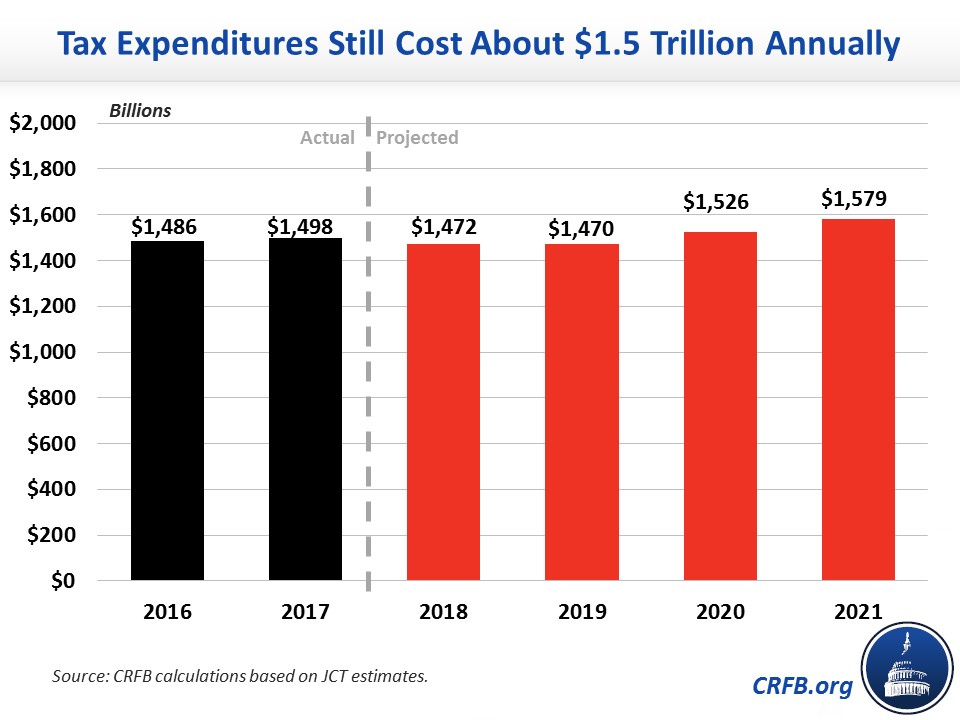

In other words, “tax expenditures” are something virtually any taxpayer, even individuals, might take advantage of. And government data bears this out. According to current estimates from the U.S. Treasury Department, the largest tax expenditures for the upcoming ten year fiscal year period from 2023 to 2032 are “[e]xclusion of employer contributions for medical insurance premiums and medical care ($3,366,320 million); [e]xclusion of net imputed rental income ($1,679,550 million); [d]efined contribution employer plans ($1,535,700 million); and [c]apital gains (except agriculture, timber, iron ore, and coal) ($1,492,400 million).” U.S. Treasury Dept., supra.

Under Plaintiffs’ argument, all taxpayers taking advantage of the multitudinous deductions, exclusions, exemptions, and other similar provisions of the tax code would likewise be recipients of federal funds, just as much as Baltimore Lutheran. While these taxpayers may not be covered by Title IX because they do not provide the educational activities or programs covered by that specific legislation (see 20 U.S.C. §§ 1681(a) & 1687), under the rationale adopted by the District Court, they are subject to being swept up in any statute that depends on receipt of federal funds for its coverage.

Importantly, though, while these provisions are accounted for as “expenditures” under federal budgetary principles, they are not in fact the same as receiving government funds. Section 501(c)(3) and other such tax provisions may provide a form of governmental benefit, but they do not provide actual money to the entity. See, e.g., Johnny’s Icehouse, Inc. v. Amateur Hockey Ass’n, 134 F. Supp. 2d 965, 972 (N.D. Ill. 2001) (“In U.S. 63, 71 (1982) (“Statutes should be interpreted to avoid . . . unreasonable results whenever possible.”). That, however, is what Plaintiffs’ theory portends. The indirect benefit derived by a taxpayer from § 501(c)(3)—or §501(c) more generally—simply cannot be considered the equivalent of a direct grant from the government without upending a settled understanding of the Internal Revenue Code and Congressional intent to promote and protect certain activities through tax law. Baltimore Lutheran’s 501(c)(3) status is therefore not “federal financial assistance” and not a basis for applying Title IX.

Another amicus brief directly addresses Bob Jones (in which the Supreme Court said tax exemption is subsidy just like direct expenditures):

On that point, the district court misread the Bob Jones decision. That decision actually cuts against the district court’s finding that tax exempt status is federal financial assistance under Title VI and IX. In Bob Jones, the Supreme Court affirmed the IRS’s policy on grounds limited to racial discrimination in education. 461 U.S. at 592. “An unbroken line of cases following Brown v. Board of Education establishes beyond doubt this Court’s view that racial discrimination in education violates a most fundamental national public policy, as well as rights of placing a discriminatory school outside the common law definition of “charitable.” Id. If 501(c)(3) status were itself federal funding, none of Bob Jones’ analysis would have been necessary. The Supreme Court simply could have held that every organization that applied for and received 501(c)(3) status voluntarily subjected itself to federal laws tied to the receipt of federal financial assistance.

Still, that same term, the Supreme Court held that the federal government’s general designation of a particular status, however valuable, is not federal financial assistance. The Rehabilitation Act of 1973, like Title VI, regulated private entities that receive federal financial assistance, and gave enforcement authority to the “agencies administering the federal financial assistance programs.” Cmty. Television of S. Cal. v. Gottfried, 459 U.S. 498, 509 (1983). The Supreme Court held that the FCC’s act of granting broadcast licenses was not such assistance, and therefore the FCC lacked such primary enforcement power. Id. Under Gottfried, federal licenses and certifications are not federal financial assistance, even when they “provide benefits that are as valuable as direct financial assistance.” Herman v. United Bhd. of Carpenters & Joiners of Am., Loc. Union No. 971, 60 F.3d 1375, 1381-82 (9th Cir. 1995). The Supreme Court’s decisions in Bob Jones and Gottfried implicitly rejected Judge Bazelon’s finding in McGlotten v. Connally, 338 F. Supp. 448, 461 (D.D.C. 1972), that the grant of 501(c)(8) status to a fraternal order was federal financial assistance. The Department of Justice argued in 1985 that McGlotten “‘has had no case law progeny,’” that McGlotten’s “discussion of Title VI and ‘federal financial assistance’ was merely ‘dictum’ in a case that was really about the state action doctrine and the equal protection clause,” and that the Supreme Court’s decision in Regan v. Taxation with Representation, 461 U.S. 540 (1983), ”‘conspicuously failed to invoke’” the McGlotten decision. Paralyzed Veterans of Am. v. C.A.B., 752 F.2d 694, 709 (D.C. Cir. 1985), rev’d, 477

U.S. 597 (1986).

Although Judge Bazelon took issue with the DOJ’s argument, no decision has endorsed McGlotten’s rationale. In recent decades, the best that any court has said about McGlotten’s view of Section 501 tax exemptions is that such an argument is not so “wholly insubstantial and frivolous” as to negate federal question jurisdiction. These holdings do not endorse McGlotten. They merely recognize that, because no decision has formally overruled McGlotten, an attorney may make such an argument without violating Rule 11 or bringing federal question jurisdiction into doubt. The DOJ continues to characterize McGlotten as an outlier: “Typical tax benefits—tax exemptions, tax deductions, and most tax credits—are not considered federal financial assistance.” Even if McGlotten’s finding had some continued relevance for 501(c)(8) fraternal organizations, its rationale cannot apply to 501(c)(3) charitable organizations generally or to independent schools in particular.

Other briefs are available via Bloomberg Law (subscription required), but I didn’t get access to the appellee’s brief, or any amici briefs supporting tax exemption as government spending. Amici Thomas Moore make a facially attractive argument that if tax exemption is subsidy, then we are all subsidized whenever we benefit from a tax concession. To which someone should reply, “that’s exactly the point,” because its true that deductions — at least those not necessary to measure income — subsidize something. Subsistence, health care, children, higher education, marriage, charitable giving, research and discovery, purchasing a home, etc. Surprise, surprise. We are all socialist benefactors in one way or another. And I gotta tell you, I get the feeling that there are no tax lawyers involved in the case. I hope some get involved because the tax expenditure issue needs wordier clarification than that offered. DOJ should intervene.

darryll k. jones