Lions and Lambs: LIHTCs and Nonprofit General Partners

Everybody should have a home. At least that much. But there is a housing crisis. I’m not talking about my wife and I living in a house with empty rooms upstairs. We are empty nesters, reluctant to sell the house because we would have to buy something smaller that might cost more. Somebody could be living upstairs for all we know. But I’m talking about homelessness, not the problems of too much house.

Everybody should have a home. At least that much. But there is a housing crisis. I’m not talking about my wife and I living in a house with empty rooms upstairs. We are empty nesters, reluctant to sell the house because we would have to buy something smaller that might cost more. Somebody could be living upstairs for all we know. But I’m talking about homelessness, not the problems of too much house.

The Chronicle of Philanthropy is running a series of stories regarding affordable housing this week. Bloomberg ran an interesting story a few days ago about exempt organizations’ efforts to coral their for-profit partners who fund affordable housing initiatives. Senate Finance held a hearing — another in a list of many — on the topic about a month ago. The hearing is entitled “Tax Policy’s Role in Increasing Affordable Housing Supply for Working Families.” You can watch the whole thing at the Youtube video below.

Its all pretty complicated but from a tax exemption standpoint it all revolves around an enduring tax exempt problem. Attracting capitalists to socialist causes without allowing capitalists to c0-opt the tax subsidized charitable activity. Under IRC 42, which last year the Sixth Circuit referred to as a “highly complex unique federal program” exempt affordable housing organizations can enter into joint ventures with banks, developers and other private investors who need shelter. The Senators and witnesses called IRC 42 the most successful affordable housing program in U.S. history. Here is Service’s 350 page single spaced explanation if you are interested in the fine details. Housing, health, and education are the big three of exempt organizations so there is much to learn from those industries as they relate to tax exemption jurisprudence. Each activity almost deserves its own subtitle because each activity deals with things subject to very lucrative market demand and, at the same time, things that are quintessentially charitable. By that I mean that housing, education and health care are indispensable to life. The provision of a thing indispensable to life, without regard to profit, yet supplied in insufficient amounts by the market is quintessentially charitable.

The problem for tax exemption jurisprudence happens when capitalist and altruists join together to simultaneously exploit the market and pursue charitable goals, each thinking they can do better with the other involved. That is what OpenAI is trying to do. Not very successfully though. It is also the reason we have so much law surrounding “whole hospital joint ventures.” The concern is that the charitable endeavor will be subsumed into the thirst for profit, when perhaps never the twain should meet. But sometimes, altruists need capital for good works, and capitalists need good works for profit. When the two come together, we put some strict rules in place to ensure each partner stays in and maintains its own lane. And when the two actually come together with government permission, the rules are decidedly in favor of the charitable purpose. After all, if its only profit investors seek, they have no business co-opting the charitable halo.

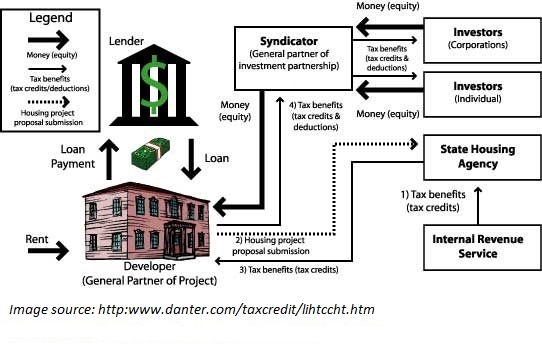

In short form, IRC 42 grants otherwise useless tax credits to exempt organizations. Useless because exempt organizations already have a 100% tax credit. They pay no taxes. Except for the tendency of transferable tax credits to shelter tax liability incurred by investors. Now there is a lure. A tax exempt housing organization with low income tax credits can exchange those credits with investors who provide capital necessary to achieve a charitable goal — like building more affordable housing. Exempt organizations join a partnership, the partnership builds and/or maintains low income housing, gets tax credits for doing so, — and here is where the transfer takes place — the partnership allocates all the tax credit to the investors. In the case linked above, the investors contributed about $9 million and over the course of the “compliance period” were allocated about $12 million in dollar for dollar tax credits. Pretty good deal. And IRC 42 ensures the charitable mission by making the credits contingent on the partnership’s making low income housing available at rents less than market value essentially. So there is almost an absolute bar to the profit motive taking over the charitable motive. No need for all that governance detail required in whole hospital joint ventures because the “profit” is accessible only if the rents are low. Beneath the picture is a more detailed description of how its works from the case linked above:

A typical arrangement under LIHTC proceeds as follows. See generally Off. of the Comptroller of the Currency, Low-Income Housing Tax Credits: Affordable Housing Investment Opportunities for Banks 6-9 (Mar. 2014), https://www.occ.gov/publications-and-resources/ publications/community-affairs/community-developments-insights/pub-insights-mar-2014.pdf (providing general overview of the mechanics of LIHTC). A low-income housing developer first applies to a state housing credit agency for an award of federal tax credits. If the state agency grants the application, the developer then enters into a limited partnership as a general partner with a private investor as a limited partner. Often, the investor is a bank or another financial entity that has ample annual tax liability of its own that makes acquiring the nonrefundable tax credits a worthwhile investment. The limited partner investor then provides the capital needed to build and develop the low-income housing development. In return, the partnership allocates the vast majority (usually 99.99%) of tax credits and other tax benefits to the investor. These benefits alone provide the investor with a significant return on investment that makes the arrangement attractive and worthwhile to the investor. See, e.g., Ernst & Young, Low-Income Housing Tax Credit Assessment Survey 6 (2009), https://www.nahma.org/wp-content/uploads/ files/member/Tax%20Credit/Legislative%20Study_FINAL%20092509.pdf (finding average annual post-tax rate of return on investment to be approximately 10%).

LIHTC allows investors to claim the tax credits through the arrangement annually over a ten-year period. 26 U.S.C. § 42(b)(1)(B) . Housing developments that receive LIHTC tax credits must comply with income-eligibility requirements and rent limits for an initial 15-year compliance period, and, for projects that began in 1990 or later, an additional 15-year extended use period. See id. § 42(h)(6)(D), (i)(1) . During the initial 15-year compliance period, the tax credits can be recaptured by the IRS if the developer violates the LIHTC requirements for the housing developments, such as certain rent or income restrictions, or if the development faces serious physical damage or financial problems. See id. § 42(j) . Beyond this initial period, however, the IRS cannot recapture any tax credit and the program is then enforced primarily by the state housing agencies. See id.

When Congress enacted LIHTC, it was especially concerned about the long-term preservation of the low-income housing developments. Recognizing that nonprofits are generally more likely than for-profit developers to maintain rents at below-market levels beyond the initial compliance period, LIHTC requires that state agencies administering the program award at least 10% of their tax credits to projects that involve nonprofit developers. See id. § 42(h)(5 ).

Alas, a lion is gonna be a lion, a shark is gonna be a shark even if lions and sharks can be characterized in cartoons as benevolent. At some point, the profiteers are gonna wanna profiteer. So when the tax credits all run out, the only thing left is the low income housing built and maintained by the partnership to which the exempt organization has contributed taxpayer subsidy. The tax credit is all gone so there is no other profit source for the investors. Predictably, the investors want what’s left after the credits dry up. They want the housing, they are sharks don’t you see? The want the housing either to jack up the rents or sell it for what little profit remains in the venture. Nonprofits responded by adopting rights of first refusal, meaning that nonprofits have the right to buy the property before anybody else and get this, at a below market price set out in the partnership agreement when the partnership is formed. The issue in the cases is that the ROFR is not triggered until the partnership gets a “bona fide” offer from a potential buyer.

Well, in order to trigger the ROFR, nonprofits enlist a third party to make an offer. The third party is never really serious about it, and the exempt organization doesn’t want to sell. The exempt org wants to hold the property to continue its charitable mission, and it wants the private investors to take their credits and be on their way (or invest in another LIHTC partnership). The third party is a classic “accommodation party” making noise so the exempt organization can keep the property forever dedicated to the charitable purpose by exercising the ROFR. Who knew exempt organizations could be so tax devious?

For-profit investors have balked at all this, challenging the ROFR on the basis that the accommodation party is not really in it to win. That is, the offer is not “bona fide.” True enough in the real world but the Courts have interpreted “bona fide” in light of the purpose of IRC 42, holding that the offer need not be enforceable, and even that the exempt organization does not ever need to really want to sell to the accommodation party. The “bona fide” offer is really one engineered by the exempt organization to get rid of the investors, whose profit making instincts threaten the charitable mission now that tax credits are all gone.

The Congress is concerned enough about the artificiality of it all that it is currently considering a piece of socialist legislation — called the DASH Act — that would just do away with the bona fide offer requirement, further weakening profiteers ability to profiteer from LIHTC “whole housing” joint ventures with exempt organizations.

The lesson is that capitalists and socialists can indeed join together but they never shed their instincts. So the law has to keep a very short lease on capitalists when that happens.

darryll jones