Excess Business Holdings, Newman’s Own, and Patagonia’s Purpose Trust

An interesting piece in the Financial Times (a subscription might be required) last weekend made me question whether the excess business holding tax is a good or bad thing. I still don’t quite believe the rationale behind IRC 4943. Here is a good overview, including a discussion of the Newman’s Own exception. And here is a brief excerpt from the Financial Times:

Capitalism is built on the profit motive. So charities are not obviously appropriate owners for businesses. But foundations, which typically have dual social and commercial goals, can be successful stewards. Denmark’s weight loss drugmaker Novo Nordisk is the best known example. Support from a foundation holding 77 per cent of its voting rights allowed it to invest in the then-unfashionable area of obesity research in the 1990s. It is now Europe’s most valuable company, having made its owner the world’s biggest charitable foundation.

Foundation-owned firms’ financial results are comparable to those of their other corporate peers, according to research by Steen Thomsen of the Center for Corporate Governance at Copenhagen Business School. They are particularly prevalent in Denmark — think Maersk and Carlsberg. Elsewhere, examples include Sweden’s Wallenberg empire, India’s Tata conglomerate, the UK’s Associated British Foods, Switzerland’s Rolex and California’s Patagonia. The latter — created in 2022 — is a rare US example, as unfavourable 1969 tax rules were only lifted in 2018.

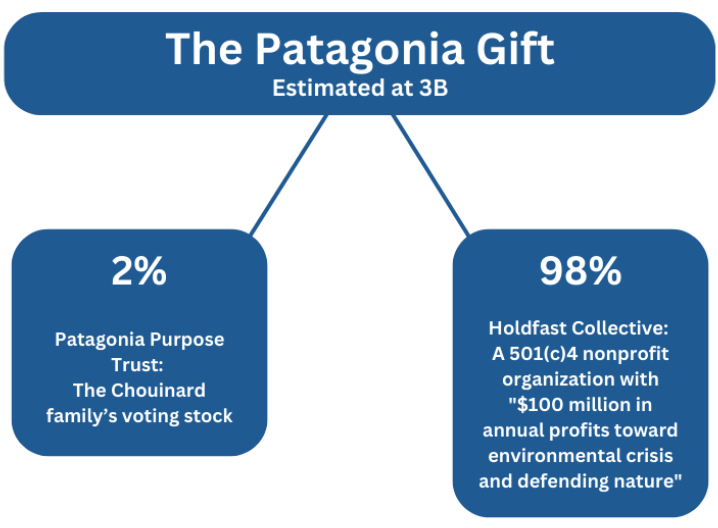

Of course, those “unfavourable 1969 tax rules” have not actually been lifted because the Newman’s Own exception is very narrow. Patagonia is effectively owned by the Patagonia Purpose Trust and might have been structured to meet the Newman’s Own exception. The Trust owns all of Patagonia’s voting stock, while the nonvoting stock is owned by Holdfast, a 501(c)(4). But it sounds as if the family owned business is still controlled by the family. If that is true then it would not meet the “independence” requirement of IRC 4943(g). Instead, Patagonia invented a workaround known as a “purpose trust.”

I don’t know much about such things, but here is an interesting article from Beck Groff and Susan Gary. As near as I can tell so far, if the trust income is distributed annually to the (c)(4), instead of a private foundation, the donors can achieve the same result allowed under the Newman’s Own exception without giving up control, as is required under IRC 4943. The upfront cost is that the gift to the (c)(4) generates no income tax deduction. But it generates a huge gift tax deduction. Dollars are dollars.

I’ve just never understood why tax law prohibits a thing with its right hand that is allowed by its left hand, but only to those who can afford the expense of an obscure tax strategy. I might just be talking about the different burdens imposed on multi-millionaires that are not imposed on multi-billionaires. Anyway, Holdfast, the 501(c)(4) is tax exempt and doesn’t have to worry about the private foundation excise taxes on excess business holdings. And though the gift to the (c)(4) didn’t generate an income tax deduction, it saved the donor about $700 million in transfer taxes. Meanwhile, the donor doesn’t have to divest itself of control as required by the Newman’s Own exception.

darryll k. jones